The EBA Climate Stress Test: The New 2027 Climate Risk Module and What Banks Should Do

The EBA Climate Stress Test: The New 2027 Climate Risk Module and What Banks Should Do

The EBA climate stress test has moved from the margins into the rulebook. The draft 2027 EBA stress test methodology now carries a dedicated section that sets out, exposure by exposure, how climate risk feeds into the exercise.

What banks need to do to prepare for the EBA stress test 2027

A practitioner checklist for climate risk in the EBA stress test 2027 falls into four workstreams:

- Data first. Geocode collateral to coordinate level, complete the mapping of non-financial corporate to NACE Rev.2, close energy performance gaps on the mortgage book, and assemble insurance coverage rates by counterparty type. Data readiness, not modelling sophistication, is what usually limits a first climate run.

- Models. Extend internal PD and LGD models to ingest the transition shocks (carbon, energy, gross-value added) and the flood-depth inputs, and re-calibrate flood damage functions away from average toward tail metrics.

- Reporting build. Stand up the new templates aligned with the provisional FINREP F49 portfolios — which have been themselves under consultation until July 10th.

- Documentation. Draft the explanatory-note narrative as you go: the shock-set choice, the flood classification approach, and every insurance assumption. The draft asks for this in writing.

Above all, read the bigger picture. Even as a P&L-only overlay with no risk-weighted asset impact, this is the first EU-wide climate risk stress test with prescribed flood mechanics and a common transition scenario. The institutions that treat the draft as a dry run will be the ones already prepared when the next EBA climate stress test arrives.

A new dedicated climate risk module

For anyone tracking the EBA stress test 2027, the message is clear. The draft EBA 2027 stress test methodology introduces a stand-alone climate risk module — a defined part of the test that prescribes, in a specific way, how transition and flood shocks are layered onto the regular adverse scenario. Climate risk is no longer assessed on the side. It is no longer a separate one-off analysis (the 2022 ECB climate stress test, for instance), nor a set of qualitative add-ons. Instead, climate risk now comes with specific, prescribed modelling steps, a deliberately defined set of exposures, and its own reporting templates CSV_CL_TR (climate transition) and CSV_CL_PR (climate physical risk). The latter one is aligned with the provisional FINREP Template F49.

Because the methodology published in June 2026 is a draft, treat every design choice below as proposed rather than fixed.

The following is most relevant for practitioners:

- how the module attaches to the core test without touching capital ratios;

- which exposures actually fall inside the scope;

- how the transition shock is built from carbon, energy and NACE-sector inputs;

- how the flood scenario is modelled off the JRC hazard maps;

- how the losses reach the P&L, and how insurance splits the result; and

- the concrete preparation steps worth starting now.

The climate risk module that sits on top of the core test

The climate risk module is an overlay. Banks apply the transition and flood scenarios in conjunction with, and on top of, the adverse macro-financial scenario of the 2027 EU-wide stress test. The climate shocks add to the macro stress; they do not offset it.

The climate module is P&L-only. It runs through credit losses, provisions and impairments, but it deliberately leaves the risk exposure amount (REA — the EBA's term for the risk-weighted-asset base) untouched. There is no separate capital requirement recalculation for climate.

The climate module does not change the headline capital depletion or the CET1 ratios that the core stress test produces. The core results stand on their own. The climate figures sit beside them as a separate, analytical read on how sensitive a bank's book is to climate shocks.

However, "no capital impact" describes the current draft, not the long-run trajectory. The module produces a structured supervisory dataset on climate loss sensitivity and that dataset is exactly the kind of input that feeds future stress-test cycles and Pillar 2 dialogue. The absence of an REA charge today is a methodological choice, not a judgement that the risk is small.

The scenarios are built by the ESRB and the ECB together with the EBA, competent authorities and national central banks. The ESRB ECB climate scenario is the common reference, so banks are not free to invent their own shock paths.

What falls inside the EBA climate stress test scope

Climate stress testing works the opposite way to a conventional macro stress test. A macro scenario stresses the entire balance sheet, because a recession touches everything. A climate scenario is targeted: transition and flood shocks only bite where the exposure is actually sensitive to them, so the EBA climate stress test scope is restricted to the portfolios where those channels transmit, and the boundaries are precise in the draft EBA 2027 stress test methodology. The module covers on-balance-sheet credit risk exposures measured at amortised cost. Market risk is explicitly excluded. There are two risk legs, and each has its own scope.

Transition risk covers total exposures — loans, advances and debt securities — to non-financial corporations (NFCs) in the climate-relevant NACE sectors (sectors A to H and M), broken down by NACE level 1 and by material NACE level 2. It also covers mortgage lending for house purchase, bucketed by the energy performance of the underlying property.

Physical risk is limited to "loans and advances": EEA exposures secured by immovable property, plus EEA non-financial corporations across all sectors.

When planning climate risk in the EU bank stress test, scoping is a data exercise before it is a modelling exercise. You need non-financial corporate exposures cleanly mapped to NACE Rev.2, a mortgage book tagged by energy-performance (EPC) bucket, and a defensible materiality cut by country. If those three are shaky, nothing downstream will hold.

Transition risk: carbon, energy and NACE-sector shocks

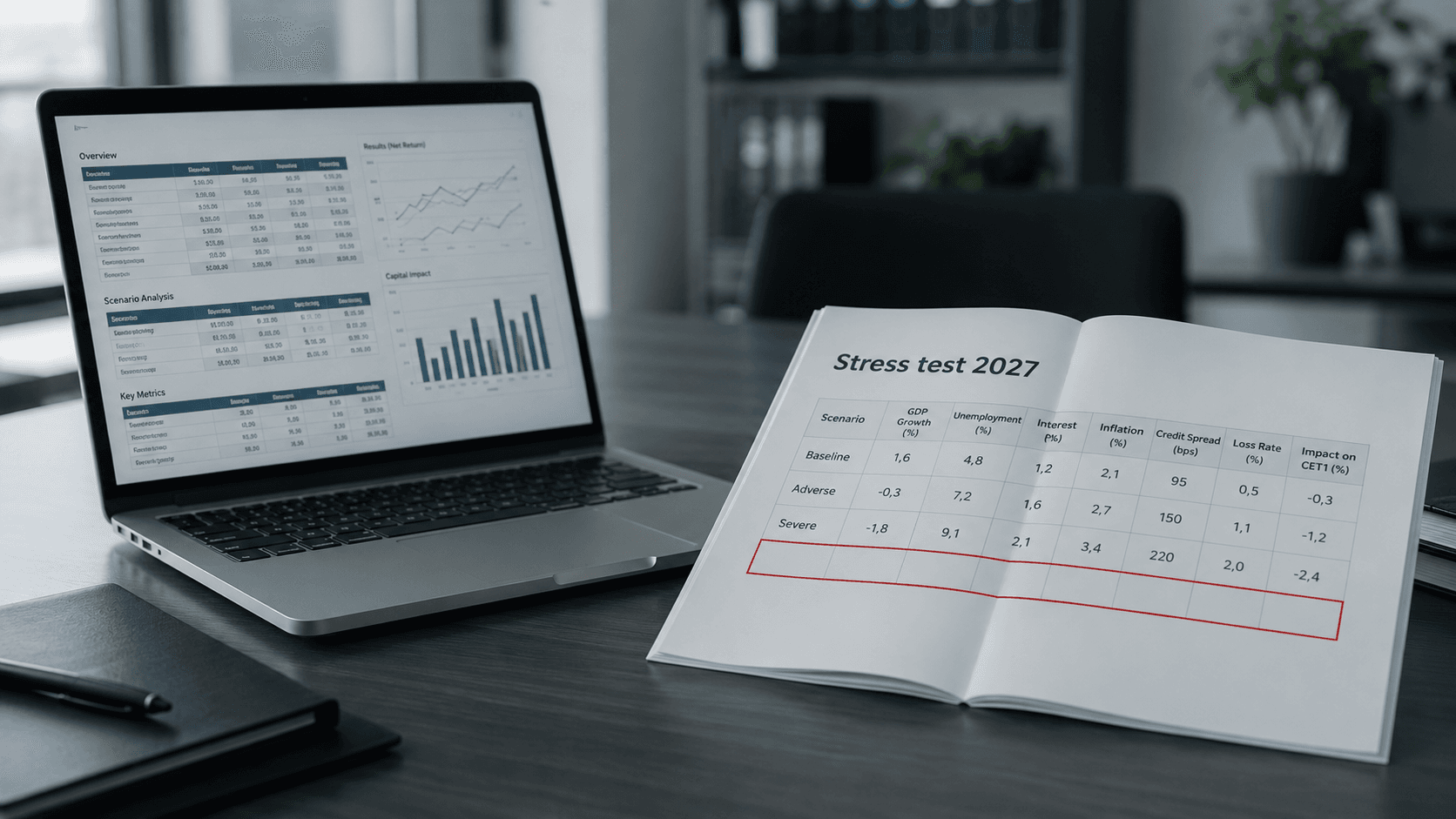

The transition leg of the EBA climate stress test runs over three years, 2027 to 2029. The scenario is defined as a sudden, stringent shift in climate policy in an unprepared, fossil-fuel-dependent economy — the kind of disorderly transition that triggers rapid capital reallocation and real-economy damage.

Banks are given two alternative sets of transition shocks and choose the one that best fits their models:

- Climate-variable shocks — carbon price pathways, country-specific greenhouse gases emission pathways, and gas and oil price shocks (aligned with the energy price shocks in the adverse macro-financial scenario of the same 2027 stress test).

- GVA shocks — sector gross-value-added stress factors at NACE 1 and NACE 2, provided by country.

The transmission channels are spelled out: banks model these inputs into borrower creditworthiness through higher operating costs, decarbonisation capital expenditure, technological substitution and shifts in product demand. For mortgages, energy efficiency feeds loss given default — energy-inefficient properties carry more transition vulnerability. The output is climate-adjusted PD and LGD projections over the three years, applied on top of an already-adverse macro path.

The choice between the two shock sets is a genuine modelling decision. The GVA route maps more directly to sector P&L; the climate-variable route asks you to build the carbon-and-energy pass-through into borrower economics yourself. Decide deliberately, and document the rationale.

Physical risk: a single flood modelled on the JRC hazard maps

The physical leg of the EBA climate stress test is a single tail event: a riverine flood with a 1% annual probability, assumed to strike all EEA countries simultaneously, in Year 1 (2027) only. There are no physical shocks in 2028 or 2029.

The hazard comes from the Joint Research Centre (JRC) river flood hazard maps, built by combining river-flow simulations, a digital elevation model, and hydrodynamic simulations of how floodwater spreads across terrain.

The EBA stress test flood risk methodology consists of the following steps:

- Geo-locate each collateral asset by latitude and longitude, and read its flood depth off the JRC map.

- Run a damage function to convert flood depth into a real-estate price shock.

- Re-value the affected collateral and push the revision into LGD in Year 1.

- Raise PDs in Year 1 for corporates located in flooded areas, allowing migration to Stage 2 or Stage 3 where credit quality deteriorates.

First, one instruction stands out because it contradicts how many banks already model floods: do not calibrate damage functions on Average Annual Damages (AAD). Because the scenario is a tail event, an AAD calibration averages the rare severe flood against many quiet years and systematically understates the loss. The draft requires tail-risk damage metrics instead.

Second, geocoding quality is the binding constraint — postcode-level data is too coarse, so coordinate-level collateral data is the real prerequisite.

Each exposure is then classified as highly, moderately or not significantly exposed, with a residual "not classified" bucket that the EBA expects banks to keep to a minimum.

From PD and LGD to the P&L and the insurance split

The whole module lands through credit risk parameters. Stressed PD and LGD drive impairments, provisions and stage transitions, and those hit the profit and loss account. The reporting flows through dedicated templates (CSV_CL_TR for transition, CSV_CL_PR for physical) and carries climate-adjusted PD/LGD projections for the in-scope exposures.

The PD/LGD climate projections come in two parallel versions — gross and net of insurance:

- Gross of insurance (as if no cover existed): report the full granular parameters; the template then computes the provisions.

- Net of insurance: report only the resulting total stock of provisions. You still use parameters internally, but no granular reporting is required.

In addition, banks report provisions net of private insurance, and separately net of private insurance plus public schemes, along with the private insurance coverage rate per counterparty type.

On the one hand, payout delays and coverage uncertainty must be reflected conservatively, with the assumptions on timing and amounts justified in the explanatory note. On the other hand, no second-round macro effects are added. Only the consolidated banking entity's losses are projected, even where a bank cross-sells insurance or owns an insurer in the group.

The gross/net split is where the analytical payoff sits. Treat the gross-to-net gap as a management metric. A large gap is a strategic exposure in its own right. It makes visible, in P&L terms, how much of a bank's projected resilience rests on insurance. Build the insurance-assumption documentation in parallel with the model.

The static balance sheet assumption holds throughout: no energy-efficiency renovations, no recovery of damaged property, and no management actions aimed at dampening climate losses within the horizon.

Frequently asked questions

How does the EBA climate stress test work?

Banks apply two prescribed climate scenarios — a disorderly transition shock and a 1% riverine flood — on top of the regular adverse macro-financial scenario of the 2027 EU-wide stress test. They translate the shocks into stressed PD and LGD parameters for in-scope exposures, and the resulting impairments and provisions flow through the profit and loss account.

Does the EBA climate stress test affect bank capital ratios?

Under the current draft, no. The climate risk module is P&L-only and explicitly leaves the risk exposure amount (REA) untouched, so it does not change the headline capital depletion or CET1 ratios produced by the core stress test. It is best read as a supervisory measurement of climate loss sensitivity rather than a capital charge.

How does the EBA climate stress test treat transition and physical risk differently?

Transition risk runs over three years (2027–2029) and covers NFCs in climate-relevant NACE sectors plus mortgage lending by energy-performance bucket. Physical risk is a single flood event applied only in Year 1 (2027), covering EEA real-estate-secured exposures and EEA non-financial corporates across all sectors.

Why does the EBA tell banks to avoid Average Annual Damages?

Because the flood scenario is a tail event, not a typical year. Calibrating a damage function on Average Annual Damages averages the rare severe flood across many quiet years, which understates the loss. The draft requires tail-risk damage metrics so the projected impact reflects the severity of a 1% event.

What is the difference between gross and net of insurance in the climate module?

Gross projections assume no insurance cover and require full granular PD and LGD reporting. Net projections reflect the expected mitigating effect of insurance and require only the total stock of provisions. Banks report net of private insurance and, separately, net of private insurance plus public schemes, with conservative assumptions on payout timing.

Which exposures fall inside the climate risk module scope?

On-balance-sheet credit exposures at amortised cost. Transition risk covers non-financial corporate (NFC) exposures in NACE sectors A–H and M (by level 1 and material level 2) and mortgages by energy-performance bucket. Physical risk covers EEA loans and advances secured by property and EEA NFCs. Market risk is excluded.

Is the EBA 2027 stress test methodology published in June 2026 final?

No. It is a draft under consultation, and the climate module — including its scope and flood mechanics — can still change.

Related articles

Continue exploring with related insights from our experts.

PD Model Backtesting in the Spotlight: What the EBA's 2026 Paper Means for European Banks

For two decades, the performance of banks' PD models stayed inside confidential supervisory channels. The EBA's April 2026 Staff Paper changes that — applying systematic PD model backtesting across EU IRB banks, sharpening the binomial test for both asset and serial correlation, and putting a Tier 1 capital number on the result.

Credit Risk Modeling Trends 2026: Five Shifts Risk Managers Should Prepare For

The credit risk function of 2026 looks materially different from the one most banks still operate. Here are the five shifts, from generative AI to ESG integration, that risk managers should plan for now.

Less & Faster IRB Model Changes — What Actually Changed (and Why It Matters)

How the new IRB rules transform many previously time-consuming model changes into simple notifications—thereby drastically shortening approval times and significantly accelerating implementation